Your credit score plays a crucial role in your financial health. It affects everything from your ability to get approved for loans and credit cards to the interest rates you pay. Whether you’re planning for major purchases, a new car, or a home, mastering your credit score is vital for achieving financial success. As we approach 2025, it’s essential to stay up to date with the latest tips and strategies to boost your credit score and ensure it reflects your financial responsibility. This guide will provide valuable tips on how to improve your credit score, manage debt wisely, and build a strong financial foundation for the future.

What is a Credit Score?

A credit score is a three-digit number that lenders use to assess your creditworthiness, or your ability to repay borrowed money. The score is calculated using various factors, including your payment history, amount of debt, credit history length, new credit inquiries, and the types of credit accounts you hold. The higher the score, the better your chances are of securing credit with favourable terms, such as lower interest rates and better loan terms.

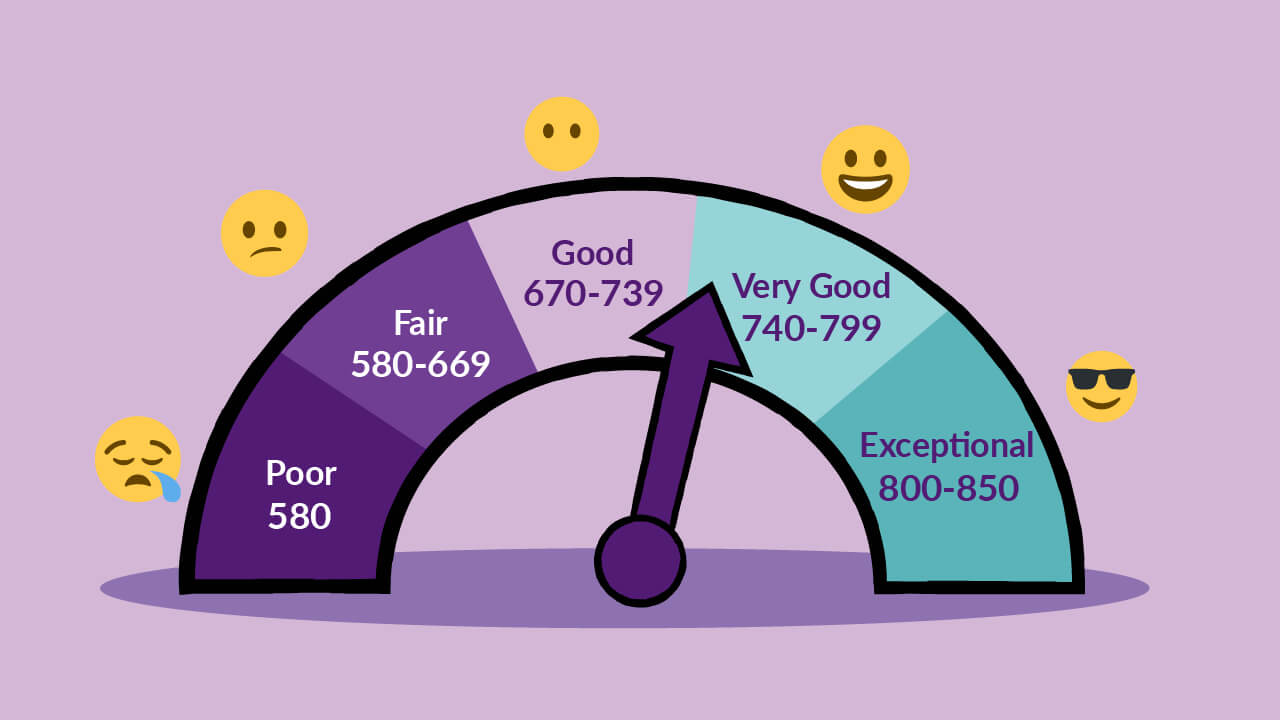

Credit scores typically range from 300 to 850, with higher numbers indicating better credit. Here’s how the credit score ranges are typically broken down:

- Excellent (750-850): Great credit score, qualifies for best terms and rates.

- Good (700-749): Solid credit, qualifies for good terms.

- Fair (650-699): Average credit, may face higher interest rates.

- Poor (600-649): Poor credit, could struggle with approval and higher rates.

- Very Poor (300-599): Very poor credit, likely to be denied credit or face very high rates.

Why Credit Scores Matter

A good credit score can help you in several areas of your financial life:

- Lower Interest Rates: Whether you’re applying for a mortgage, auto loan, or credit card, a higher credit score can mean significantly lower interest rates, saving you money in the long run.

- Loan Approval: Lenders are more likely to approve loans for individuals with higher credit scores.

- Better Insurance Premiums: Some insurers use credit scores to determine premiums. A better score can lead to lower premiums.

- Employment Opportunities: Certain employers check credit scores as part of their hiring process, especially for positions that involve financial responsibilities.

- Security Deposits: Landlords and utility companies may require a security deposit if your credit score is low. A higher score can reduce or eliminate these costs.

Tips to Master Your Credit Score in 2025

Improving and maintaining a strong credit score requires time, diligence, and the right strategies. The following tips will help you take charge of your credit score and boost your financial health.

1. Check Your Credit Report Regularly

Your credit score is derived from information found in your credit report. It’s important to review your credit report regularly for accuracy. Mistakes, such as incorrect account information, late payments that were paid on time, or unauthorized inquiries, can negatively impact your score. You’re entitled to a free credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—once a year. However, you can also check your credit report more frequently through services that offer free monitoring.

If you find discrepancies, dispute them directly with the credit bureau. Correcting errors can significantly improve your credit score.

2. Pay Your Bills on Time

Payment history is one of the most important factors in determining your credit score, accounting for about 35% of your score. Late or missed payments, especially those that are reported to the credit bureaus, can have a negative impact. One of the easiest ways to boost your score is to ensure you pay all bills—credit cards, loans, utilities—on time. Setting up automatic payments or reminders can help you stay on track.

3. Pay Down High Balances

Credit utilization—the ratio of your credit card balances to your credit limits—plays a big role in your credit score. Ideally, you should aim to keep your credit utilization below 30%. If your balance is close to the limit, consider paying it down as quickly as possible. High utilization signals to creditors that you may be overextending yourself financially, which could hurt your creditworthiness.

4. Don’t Close Old Accounts

The length of your credit history is another factor that influences your score. Closing old accounts may seem like a good idea to simplify your financial life, but it can lower your score. A longer credit history demonstrates that you’ve managed credit responsibly over time. If you no longer use an old credit card, keep the account open and use it occasionally to maintain your credit history.

5. Be Cautious With New Credit Applications

Each time you apply for credit, a hard inquiry is made, which can temporarily lower your credit score. While it’s important to maintain access to credit, avoid opening too many new accounts at once. This can signal to lenders that you may be taking on too much debt. Instead, focus on maintaining your current accounts and only apply for new credit when necessary.

6. Diversify Your Credit Mix

Lenders like to see that you can handle a variety of credit types, such as credit cards, mortgages, and instalment loans. A diverse credit mix can improve your credit score, but it’s important not to open accounts unnecessarily. Only take on new types of credit if you truly need them, and make sure to manage them responsibly.

7. Consider a Secured Credit Card

If you have a low credit score or no credit history, a secured credit card may help you rebuild or establish credit. A secured credit card requires a cash deposit as collateral, which acts as your credit limit. By using the card responsibly and paying your balance in full each month, you can build a positive credit history. Over time, you may be able to upgrade to an unsecured card with better terms.

8. Use Credit-Building Tools

In addition to traditional credit cards, several tools can help you build or improve your credit score:

- Credit-builder loans: These are small loans designed to help you establish or rebuild credit. The amount you borrow is held in a savings account until the loan is repaid, after which the funds are released to you.

- Authorized user status: If someone with a good credit score adds you as an authorized user on their account, you can benefit from their positive payment history.

- Rent and utility payments: Some services allow you to report your rent and utility payments to credit bureaus, which can help boost your score if you’ve been making on-time payments.

9. Work With a Credit Counselor if Necessary

If you’re struggling with debt and your credit score is suffering, consider working with a reputable credit counsellor. Credit counsellors can help you develop a plan to manage your debt, negotiate with creditors, and provide guidance on rebuilding your credit. Avoid working with credit repair companies that promise quick fixes, as they may engage in fraudulent practices.

10. Avoid Bankruptcy if Possible

Bankruptcy can remain on your credit report for up to 10 years, and it can drastically lower your credit score. While bankruptcy can provide a fresh start, it should be considered a last resort. If you’re struggling with debt, explore other options, such as debt consolidation or negotiating with creditors, before filing for bankruptcy.

11. Monitor Your Credit Score

Numerous free credit monitoring services allow you to track your score throughout the year. Monitoring your credit score regularly can help you understand what actions positively or negatively impact your score. In 2025, many credit card companies and third-party services offer tools to help you track your score and give tips on improving it.

12. Be Patient

Improving your credit score takes time, especially if you’re starting from a low point. Building a solid credit history requires consistency and patience. While your efforts may not yield instant results, maintaining good credit habits will pay off in the long run, leading to a healthier credit score and better financial opportunities.

The Road to a Better Credit Score in 2025

As we move into 2025, it’s important to recognize that your credit score is not static—it’s a dynamic reflection of your financial habits. By implementing these strategies, you can gradually boost your score, improve your financial health, and secure more favourable terms when applying for loans or credit. Regular monitoring, responsible use of credit, and a focus on timely payments are the cornerstones of mastering your credit score.

Budgeting Hacks for 2025: How to Stretch Your Dollars Further

Whether you’re just starting to build credit or looking to improve an existing score, the steps you take today can have a profound impact on your financial future. Stay disciplined, stay informed, and keep your credit health in mind as you navigate your financial journey in 2025.